This document provides an overview of three types of embodied carbon reduction targets, and also examples of corporate and other voluntary commitments to reduce embodied carbon. More information about opportunities for addressing embodied carbon with policy can be found in the Carbon Leadership Forum’s Owner Toolkit.

Version: May 3, 2021

Target-setting is key to success and momentum

Investor, developer, building owner, and tenant policies are essential to reducing embodied carbon by spurring action before a project begins when the largest range of solutions are available. As a project progresses, the range of options is reduced. Setting net-zero embodied carbon targets early in a project (preferably before it begins) is therefore key to maximizing reductions and minimizing costs.

When it comes to targeting net-zero embodied carbon, there are three relevant types of targets:

- Company or organization-wide targets;

- Project-level targets; and

- Material-level (procurement) targets.

Organization-wide targets are most effective at accelerating action through aligning teams across an organization that may otherwise be siloed, such as sustainability, real estate, and procurement. Project and procurement targets support broader goals and ensure that reductions opportunities are followed through the value chain and communicated as a priority across the large number of stakeholders across a typical project.

Public sustainability commitments can also help maintain momentum on climate action within a company while signaling demand for low carbon solutions, inspiring a “race to the top” among organizations competing to be the first to net-zero.

Embodied Carbon and Scope 3 Emissions

Embodied carbon refers to the greenhouse gas emissions associated with the manufacturing, transportation, use, and disposal of building materials used in construction.

The Greenhouse Gas Protocol Corporate Accounting and Reporting Standard splits GHG emissions into three scopes:

- Scope 1 emissions are from a company’s operations that are under a facility’s direct control, e.g., on-site fuel combustion;

- Scope 2 emissions are from usage of electricity, steam, heat and/or cooling purchased from third parties; and

- Scope 3 emissions are upstream and downstream value chain emissions, including upstream supply chain emissions from purchased products, transport emissions, and business travel and downstream emissions from transport of products, usage of sold products and product disposal.

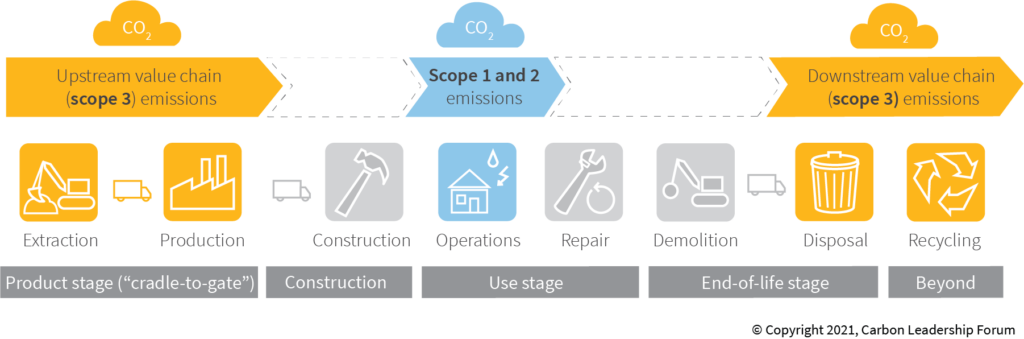

Upfront or “cradle-to-gate” embodied carbon refers to embodied carbon impacts up to the point of purchasing, and are therefore accounted as scope 3 emissions (see Figure 1). The primary categories of scope 3 emissions associated with embodied carbon are (1) purchased goods and services and (2) capital goods, or assets that are used to produce goods or services.

Figure 1. Building product life cycle stages included in scope 1, 2, and 3 greenhouse gas accounting, as described by the Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Reporting Standard. Cradle-to-gate emissions (including extraction, transportation, and production) as well as end-of-life waste disposal and recycling emissions are included in scope 3 emissions. Other life cycle stages, such as construction and demolition, are not clearly attributable to a category.

Setting Project and Material Embodied Carbon Targets

Project-level targets

Project-level embodied carbon targets should be set before a project begins and communicated in owner’s project requirements. There are two primary approaches to setting project-level targets:

- A carbon intensity limit sets a maximum carbon footprint per area value for a building. For example, the Zero Carbon Certification requires that “[t]he total embodied carbon emissions of the project must not exceed 500 kg-CO₂e/m².”

- Percent reduction goals from a baseline value can be set for the entire project or on a per area basis. For example, the LEED v4 credit “Building life-cycle impact reduction” awards points to teams that “conduct a life-cycle assessment of the project’s structure and enclosure that demonstrates a minimum of 10% reduction, compared with a baseline building.”

The embodied carbon of a project can be calculated by using whole building life cycle assessment (WBLCA) tools, such as Tally, OneClickLCA, and others. WBLCA analysis should be included in the scope of work for the project, to be led by the architect, engineer, and/or sustainability consultant. Learn more about WBLCA in the Carbon Leadership Forum’s Practice Guide.

Analyzing data from past projects is ideal for providing meaningful carbon intensity limits or reduction goals. As of April 2021, there is no publicly available database of building life cycle assessments to provide embodied carbon benchmarks at the building scale. The Embodied Carbon Benchmark Study compiled over 1000 buildings to establish consensus on the order of magnitude of typical building embodied carbon. Additional research is needed to provide benchmark numbers similar those available for operational energy.

Material-level targets

Procurement targets should be set during the design process and included in specifications. Similar to project-level targets, two approaches can be used:

- A material carbon intensity limit sets a maximum carbon footprint per unit of material, such as a cubic yard of concrete. For example, the State of California requires that rebar purchased for State projects must be below the global warming potential limit of 1.06 metric tons CO2e per metric ton of rebar.

- Percent reduction goals from a baseline value can be set in total or per functional unit of material. For example, the LEED BD+C New Construction pilot credit “Procurement of Low Carbon Construction Materials” awards teams 1 point for reductions of 0-30% and 2 points for reductions above 30% from the Carbon Leadership Forum’s Material Baselines values.

Product embodied carbon should be tracked via product-specific environmental product declarations, rather than whole building life cycle assessment tools. Learn more in Procurement Policies to Reduce Embodied Carbon.

Voluntary Embodied Carbon Commitments

While many building owners may choose to develop embodied carbon targets as part of broader initiatives like Science Based Targets or their corporate green building policies, the 2030 Challenge for Embodied Carbon and the Clean Construction Declaration are two examples of commitments that include targets specific to embodied carbon in construction.

![]()

The 2030 Challenge for Embodied Carbon from Architecture 2030 asks the global architecture and building community to adopt the following commitment:

The embodied carbon emissions from all buildings, infrastructure, and associated materials shall immediately meet a maximum global warming potential (GWP) of 40% below the industry average today. The GWP reduction shall be increased to:

- 45% or better in 2025

- 65% or better in 2030

- Zero GWP by 2040.

Signatories to the Clean Construction Declaration from C40 Cities pledge to “bring together and inspire stakeholders to take action, and enact policies and regulations where we have the powers to:

- Reduce embodied emissions by at least 50% for all new buildings and major retrofits by 2030, striving for at least 30% by 2025

- Reduce embodied emissions by at least 50% of all infrastructure projects by 2030, striving for at least 30% by 2025

- Procure and, when possible, use only zero emission construction machinery from 2025 and require zero emission construction sites city-wide by 2030.”